ClearCheckbook officially turns 20 years old on May 20th, 2026! It’s incredible to think back on the last 20 years and see how ClearCheckbook started and what it’s developed into. We’re also launching a special anniversary premium promotion, so be sure to read through the post to find out more.

From a Project in College to the "Aha" Moment:

Back in 2005, I was nearing graduation from college and was starting to face the reality of my finances. While they were fairly basic back then with just a checking account, savings account and one credit card, I was having trouble finding a tool to help me track my spending. In those days, there really weren’t any online tools for managing your finances and all of the downloadable software was geared more towards people with much more complex finances.

Since I was going to school for graphic design with a focus in interactive multimedia, plus a minor in computer programming, I decided to build myself a financial management tool that worked the way I wanted it to. One that wasn’t overly complex and could run as a website.

For about a year, the yet-unnamed financial tool was running on my laptop purely for my own personal use. I had built some basic reporting tools as well as the ability to reconcile my transactions (a feature I originally called "Jive"). It worked well for my needs and helped me get a better understanding of where my money was going.

After graduating, I continued working for my university while applying for jobs. At some point, I looked at my spending reports and saw several months in a row where my expenses outweighed my income. I knew this wasn’t sustainable and sent some screenshots of these reports to some friends on an internet forum.

To my surprise, they weren’t asking me about my financial situation; instead, they were asking what tool I used to generate the reports and how I was tracking my info. This was the proverbial “aha” moment. After a week of updating the site to allow people to create accounts, coming up with a name, and finding a hosting provider, ClearCheckbook officially launched on May 20, 2006.

Powered by You:

ClearCheckbook quickly gained traction with people who were looking for a security and privacy-focused financial management tool. As more people joined, the feedback and suggestions started flooding in.

I was able to quickly integrate many of these suggestions into tools everyone uses daily, such as reminders, the credit card tool, and importing/exporting transactions. We even had cool features like “CheckBot,” which let you add transactions via SMS, a Mac OSX dashboard gadget, and an iGoogle widget. Back before Apple revolutionized mobile apps, these were easy ways to add transactions and see your balances without having to open the main site.

ClearCheckbook continued to grow, and as we grew, so did our hosting needs. We moved from a small shared hosting plan to larger private plans, to a dedicated private server, and finally to a cloud hosting provider. Each progression in our hosting services led to a faster and more robust site, which in turn led to more customer satisfaction and word-of-mouth growth.

Some of our customers from those early days are still with us and we’re forever grateful for your support.

Going All In:

For the first few years after launch, I juggled a full-time job during the day while working on ClearCheckbook in the mornings and evenings. In early 2009, shortly after the release of ClearCheckbook Premium, I started thinking about what it would mean to do this full time.

The company I was working for was starting to show signs of cracking due to the 2008 financial crisis. To prepare for the worst, I started waking up at 3 AM, working on ClearCheckbook for three hours, going to my day job, coming home, going to bed, and doing it all over again. I did this for several months, knowing that if I could push out enough updates, I could potentially take ClearCheckbook on as my sole income.

And that’s exactly what happened. By late 2009, the company I was working for filed for bankruptcy, leaving me at a crossroads: find a new job, or jump into ClearCheckbook full time. At the time, ClearCheckbook’s revenue was only a few hundred dollars a month, but I had faith in the site. I had a little nest egg saved up from pinching pennies over the previous six months and figured it could last me a year without any real income if I was extremely frugal.

Without a day job taking up my time, I poured all of my attention into ClearCheckbook. The amount of work I put into the site was significantly more than it had ever been, allowing me to launch many new features like the Dashboard, and most notably, the PalmOS app and a mobile-optimized website for the early versions of the iPhone and Android.

Two Decades in Data:

Fast forward through several new versions, full app rewrites, and a massive amount of new tools, and you arrive at today. ClearCheckbook now has around half a million customers managing over 210 million transactions. The website sees about 2.5 million pageviews each month, while the iOS and Android apps have tens of thousands of installs.

To say "Thank You" for 20 amazing years, we’re offering a special 20% off promotion if you upgrade to a monthly ClearCheckbook Premium membership during the month of May. This means you get access to all 70+ Premium features, tools, and settings for just $4 per month. The best part? This discounted rate is locked in for as long as your membership remains active.

To claim this promotion, just log into your account and check out the banner at the top of the page. If you don’t already have a Premium membership, you’ll see a button to learn more and upgrade.

The Future of Your Finances:

Our goal has always been “Money management made easy.” As we continue to develop new features and gradually freshen up the user interface, your feedback will remain our guiding light. We are deeply committed to making sure that any visual improvements to the site and apps will feel natural, intuitive, and maintain the seamless flow you already know and love.

Having just talked about your feedback helping to direct the future of ClearCheckbook… if you have some new features or tweaks you’d like to see in the site or apps, please reach out and let us know! We’d also love to hear how ClearCheckbook has helped you in your financial journey! Leave us a comment below or send us an email to share your story.

Thank you for an incredible 20 years. Here’s to many more in the exciting journey that is ClearCheckbook.

Brandon OBrienWe're currently testing dark mode for both the iOS and Android apps and hope to have it released for everyone soon.

Dark mode will be available to anyone with a premium membership (mobile or full) once it's released to the public. If you'd like to test it out now, it's available in our beta testing channels. Links to join the beta testing groups can be found below:

We're looking for feedback on how dark mode looks on various devices and if we need to update any colors to make the app look better in dark mode.

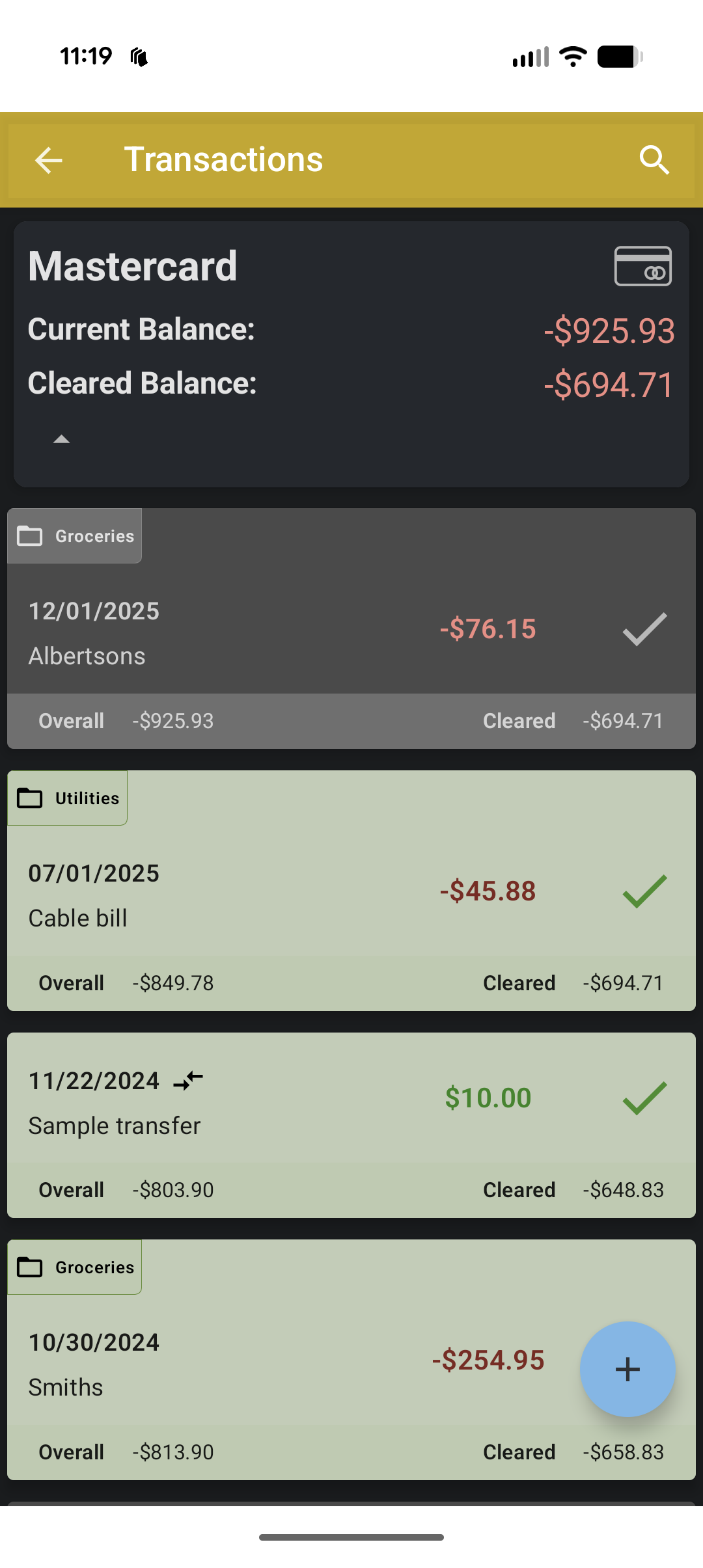

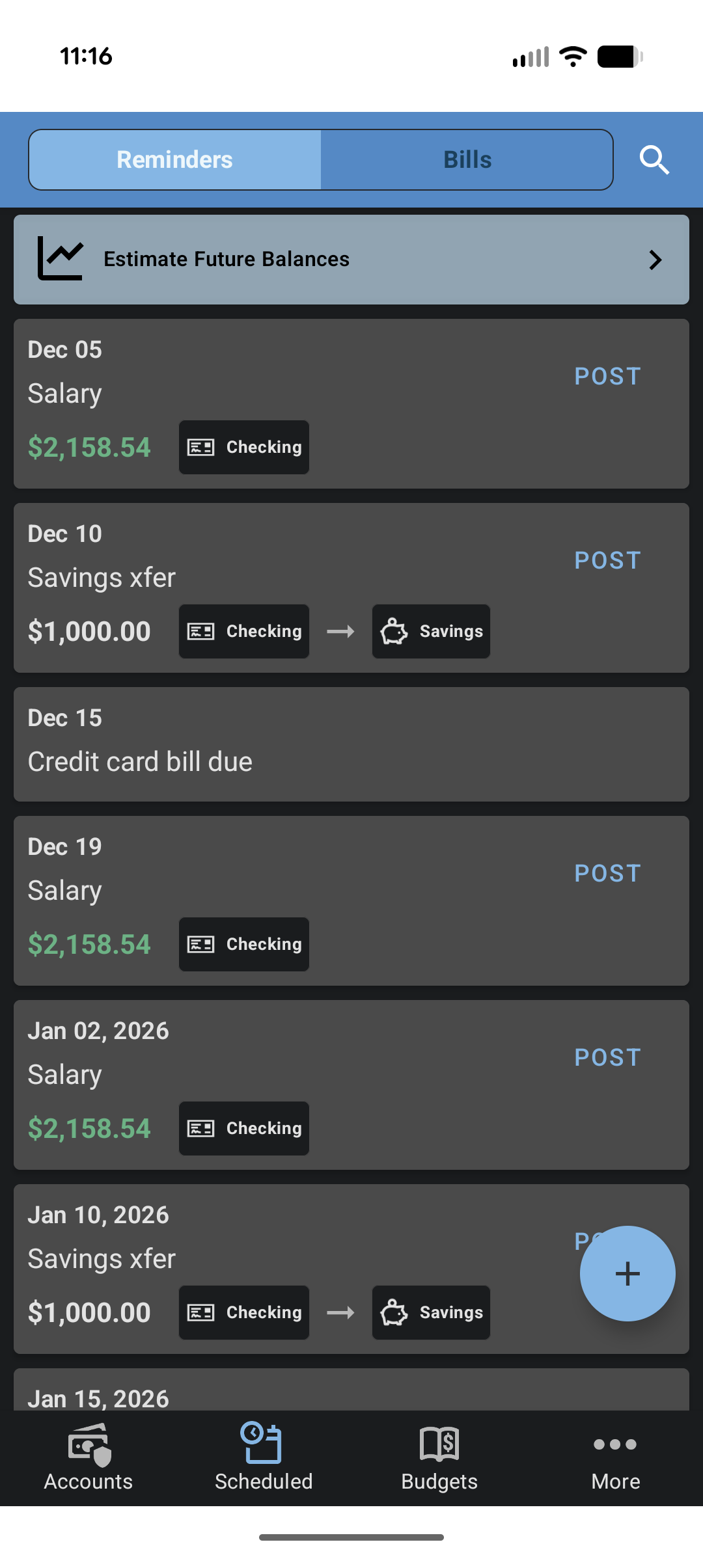

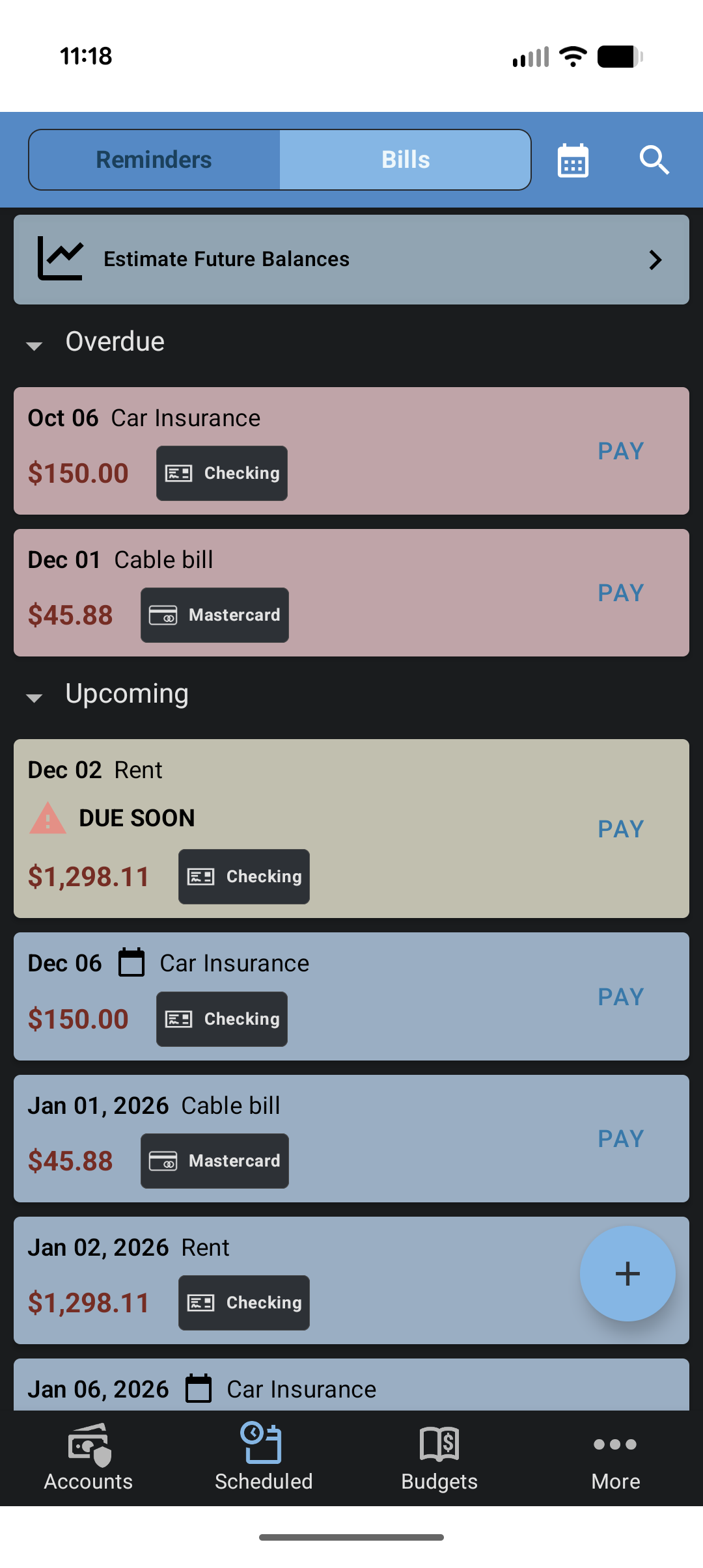

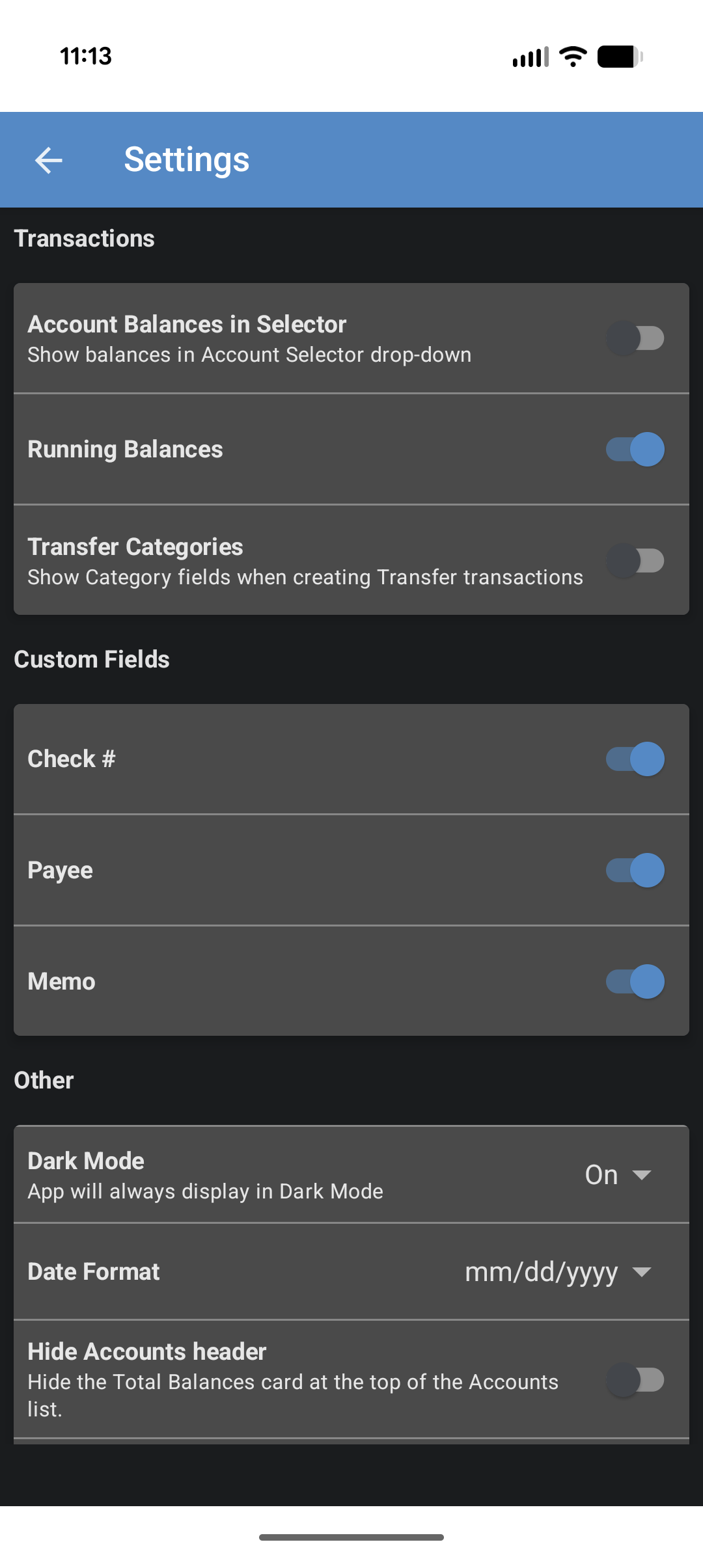

Some sample screenshots of dark mode:

Account Overviews |

Transaction list |

Reminders tab |

Bills tab |

Budgets |

Settings |

Financial scams are ever-evolving, with scammers using sophisticated methods to exploit people’s trust, create urgency, or take advantage of confusion. We’ve been hearing a lot of first hand accounts from our customers about various financial scams and wanted to post this to help others be aware of them.

Here are some of the most common scams to be aware of, including details on how they operate and tips to recognize and avoid them:

Staying informed and vigilant is your best defense against financial scams, which increasingly rely on social engineering and urgency to succeed.

Remember that ClearCheckbook will never reach out to you asking for any private information such as bank account or credit card numbers, or promising to deliver you money of any kind.

With Intuit shutting down Mint, we've had a lot of people find ClearCheckbook to replace their financial management software. We know it's always difficult transitioning from a software you're familiar and comfortable with to a new one, but we hope this blog post makes that transition to ClearCheckbook easier.

First off, welcome to ClearCheckbook! We've been helping people manage their finances since 2006 and have grown tremendously over the years, due in large part to feedback and suggestions from our customers. ClearCheckbook is free to sign up and use, but we do have a Premium Membership option that gives you access to over 70 features, tools and settings that aren't available with the free membership. Here are some common questions and answers from Mint customers:The term Jiving has been replaced with Clearing to help avoid confusion about the reconciliation process.

When ClearCheckbook was first founded back in 2006, we had used the term Jive (a homonym for jibe/gibe, to be in accordance), but over the years this has lead to a lot of confusion about what it actually meant and what the purpose was. To make things a little clearer, we're changing Jive/Jiving/Jived to Clear/Clearing/Cleared. This will make it more apparent what the term is and help make the reconciliation process easier for new customers.

Nothing has changed as far as the process for clearing your accounts and transactions go, it's just the naming that has been updated. If you're used to the jiving process, just keep an eye out for the updated terminology.

The website has been updated and we'll be working on getting the mobile apps updated soon.